Behind all household purchase is a big financial venture. Much more the past several years, co-ownership is more widespread, and joining up with members of the family otherwise nearest and dearest. not, focusing on how we are towards the home financing try important to deciding what you can reach to one another, and you may things to thought before you diving in the.

Based on JW Surety Securities, almost 15% off People in the us surveyed enjoys co-purchased a house with a person except that its close companion, and something forty eight% do consider it. Due to the fact joint mortgage loans bring numerous positives, he’s an attractive substitute for some-monetary obligations try mutual, borrowing stamina is increased, and big money which have finest interest rates is alot more achievable whenever pooling info which have a different people.

To higher comprehend the ins and outs of co-borrowing from the bank, co-finalizing, or co-buying, let’s determine two things, such as the combined mortgage.

Insights Joint Mortgage loans

A mutual mortgage try a home loan arrangement that have two different people inside it. New individuals signing the mortgage is actually discussing responsibility to your financing payment. Observe that it is distinct from shared control, which is either regularly prevent place one individual into financing because of a diminished credit rating (to track down a far greater interest and you will qualify for a higher loan amount). One user’s term will look with the home loan, regardless of if each party theoretically own the resource.

A means to Grab Name With Numerous CO-Consumers

Renters in keeping. All of the co-debtor was an owner, but for every show tends to be marketed centered on simply how much it set out for the deposit or simply how much it contribute with the monthly homeloan payment.

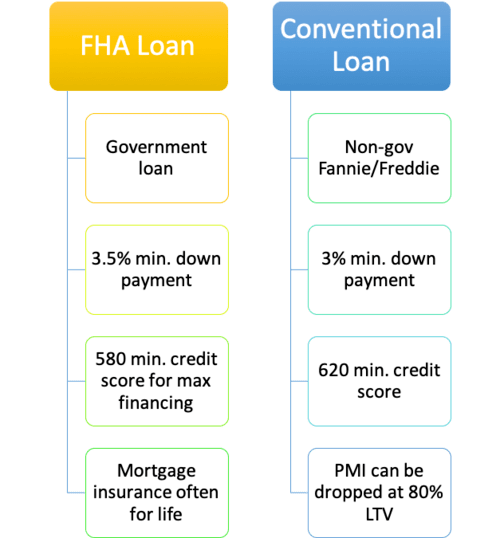

Mortgage Qualification getting Shared Candidates

The process of trying to get a shared financial is much like the method you might assume if you were taking right out home financing alone. The financial institution takes under consideration all cash: your credit score, earnings, employment background, as well as your established bills. The lender commonly thought everyone’s credit rating to choose which loan the group will qualify for.

Differing people wishing to get on the loan must complete a great separate software.But how many people should be to your financing, precisely?

Exactly how many Anyone Shall be For the Home financing?

Normally, no more than four to five co-consumers are usually enjoy into the a home loan. From the app employed by Federal national mortgage association and Freddie Mac computer, the new limitations is basic in lieu of legal. There might be, theoretically, significantly more consumers on one financing for people who discovered a loan provider in order to underwrite the mortgage without the need for one to limited application. But not, extremely loan providers will not meet or exceed four co-consumers to own a normal financing.

It might be more importantly to consider the fresh new court and logistical areas of integrating that have numerous people with the home financing.

Considerations In advance of CO-Borrowing

Before signing on dotted range, believe a lot of time and difficult regarding ramifications out-of mutual possession and you may mutual obligations. How good what are those people you may be co-borrowing from the bank with? Since the everyone’s financials grounds toward recognition, you to definitely outlier you may bring down the amount you could potentially obtain or produce a diminished rate of interest, causing the general cost along side life of the loan.

On the reverse side of the coin, Several co-consumers on a single loan can work better of these in the place of since far monetary stability and you can high credit rating-making it possible for them entry to the brand new homeownership street. At the same time, a team could submit an application for a much bigger loan amount to spend for the a multiple-tool building to reside in and book for couch potato money.

Legally, co-borrowing are challenging. Eg, an effective once-partnered couples experiencing a divorce case can now need to either offer your house, buy out the most other mate, or split up the new proceeds out-of leasing.

Generally, if an individual co-borrower desires out (otherwise has passed away), the remainder co-borrowers must determine the next procedures to each other. Which could include to get them out, offering their display, otherwise refinancing having its title taken off the borrowed funds-then you may end up with a high notice speed.

How does Cosigning Affect Your Borrowing from the bank?

Basically, are a great cosigner is able to affect your credit. The new cluster you happen to be cosigning to possess make a difference your credit rating that have their fiscal duty. If they are punctually having mortgage repayments, their get might have to go upwards. On the other hand, if a knockout post they are late or trailing into the mortgage payments, the rating might have to go off.

Difference between A CO-SIGNER And you can A CO-Borrower

To loan providers, there isn’t a big difference ranging from good co-signer and you will an excellent co-borrower-these are typically one another fiscally in charge, both foundation with the qualifying loan amount and interest rate, and you will both would be liable when the payments are not generated timely.

Yet not, if you are deciding on feel a beneficial co-borrower, this means your name’s towards the deed, while cosigners won’t be named to the deed towards the possessions. A co-signer isnt region-proprietor.

Strategies for Enhancing Borrowing from the bank Fuel

If you are considering that have multiple people into that loan, you might considerably improve mortgage qualifications to own combined candidates-both you and those individuals you spouse withbining profits can get assist you is also take on a more impressive mortgage. Along with, mutual credit ratings are usually averaged. In the past, a reduced credit history is tend to focused on many, nevertheless now, loan providers be ready to average from the credit scores so you’re able to see a happy average of all the fico scores.

However, think about the borrowing from the bank profiles, incomes, and you can property of your co-individuals seriouslymunicate really and sometimes up to your financial earlier in the day, establish, and you can coming discover a far greater thought of where you you are going to homes if you want to sign a shared mortgage loan. Bear in mind: With more someone comes so much more viewpoints plus financial complications so you can go through.

If you are happy to discuss shared financial solutions, get in touch with the newest PacRes mortgage gurus today to own individualized pointers and you may alternatives that suit your position-therefore the means of your co-borrower otherwise co-signer!

Comment closed!